Rent's due before you get paid

Landlord wants it on the 1st. Your direct deposit hits the 5th.

Tap wages you've already earned to cover the gap — then repay when your check lands.

Access wages you've already earned. See the fee upfront. Repay when direct deposit hits — bank, debit card, or Apple Pay.

Most people aren't bad with money — the timing is just off. Sound like your week?

Scroll →

Landlord wants it on the 1st. Your direct deposit hits the 5th.

Tap wages you've already earned to cover the gap — then repay when your check lands.

Groceries, gas, kid stuff — the account's getting thin and payday's still a few days out.

Get a little cushion from money you've already worked for. No borrowing next week's paycheck.

Copay, car battery, school fee — the kind of thing that doesn't wait for Friday.

Handle it with earned wages, not a panic withdrawal or a sketchy loan app.

You check your balance, but when's payroll? What hit this week? Where'd it all go?

See spending, deposits, and your next payday in one place — updated from your linked account.

Hidden fees, credit pulls, apps that make you feel dumb for asking questions.

Fee shown before you confirm. No credit check. Not a loan. Not a bank.

Autopay hits tonight. Your balance is close — and that $35 fee hurts more than the bill itself.

Bridge the gap with wages you've already earned so you stay above zero until payday.

That's the gap Zivo is built for — access to wages you've already earned, plus a straight read on what's coming in, going out, and when you get paid next.

Zivo bridges the gap between when you earn money and when it lands in your account.

Early access when you need it. Spending and deposits when you want the full picture.

Scroll →

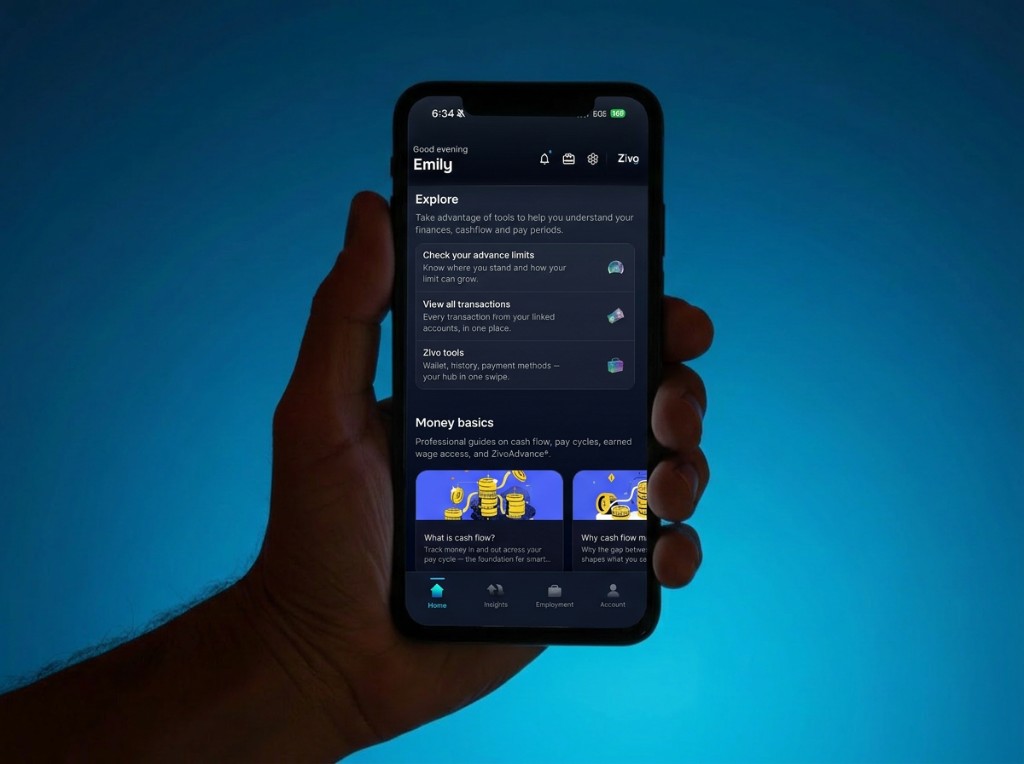

Earned wage access

Up to $200 of wages you've already worked for. Fee shown upfront. Same-day delivery when eligible.

Spending & income

Categories, deposits, and cash flow — so you're not guessing what's left before Friday.

Bank, card, or Apple Pay

Settle up on your payday. Clear breakdown, your choice of payment method.

No interest, no credit check, no payday-lender games. Here's the short version.

What it is

Early access to wages you've already earned — tied to your real pay schedule.

What it's not

Not a payday loan. No interest. No credit check. No APR math.

How it works

Pick an amount, see the fee, confirm — then repay when direct deposit hits.

Four moments most members recognize — from rent due to payday landing.

Payday's still four days out.

You're fine — but there's not much room to spare.

Check what you've earned, see the fee, take what you need.

Repay on your schedule. Back on track.

That's most working Americans — and there's nothing wrong with needing better timing.

Hourly, salaried, or gig — if you get a regular paycheck, this is for you.

When due dates and pay dates don't match up (and they usually don't).

Anyone who's ever counted days until Friday and hoped nothing else breaks.

People who want to see their money clearly — not just move it around in a pinch.

Free on iPhone and Android. Link your bank, see your fee upfront, and access wages you've already earned.

Link your bank, see your fee before you confirm, and access wages you've already earned — on iPhone and Android.

Zivo Cash Advance provides earned wage access, not a loan. Eligibility required. Fees apply before you confirm. Not a bank.

Get paid before direct deposit. See where your money goes. Repay on your schedule.

RISE DIGITAL FINANCIAL CORP

Summary for the Zivo product page. The complete disclosure notice is published at https://risedfc.com/zivo/disclosures. Read together with the Terms of Service.

Purpose, Scope, and Corporate Operator Identity

These disclosures summarize the corporate operator position of Rise Digital Financial Corp ("Rise," "we," or "us") regarding Zivo: Cash Advance and ZivoAdvance® earned wage access. They are published on Rise's marketing website for transparency to consumers, regulators, and partners. They supplement and should be read together with the Zivo Terms of Service, Privacy Policy, and all agreements and transaction-specific disclosures presented in the Zivo: Cash Advance mobile application before You confirm an advance.

Rise Digital Financial Corp is a Florida-incorporated fintech software company headquartered in Miami, Florida. Rise designs, develops, and operates Zivo: Cash Advance, distributed on the Apple App Store under Bundle ID com.risedigital.zivo, through which eligible consumers may access ZivoAdvance®, Rise's earned wage access product. Rise affirmatively states that it is not a bank, not a lender, not a money transmitter within the meaning of Section 560.103, Florida Statutes, and not a deferred presentment provider within the meaning of Section 560.402, Florida Statutes. Rise does not hold a bank charter and is not insured by the FDIC or NCUA.

Product Operator Model and Principal Transaction Structure

Rise operates as a product operator within the established fintech model. Rise builds and operates the software platform, sets eligibility criteria, advance amounts, fee structures, and repayment terms, manages the consumer relationship, and maintains the product's compliance posture. Rise is the origin of advance funds and the principal in both legs of each ZivoAdvance® transaction: Rise sends its own operating funds to the consumer on advance and collects repayment owed to itself on repayment.

At no point does Rise receive money from a consumer for the purpose of transmitting that money to a third party, act as an intermediary between a sender and recipient, or hold consumer funds in suspense pending transmission to another party. Regulatory classification turns on Rise's product structure and the consumer's actual repayment path, not on the identity of any particular third-party data vendor.

Nature of ZivoAdvance® — Earned Wage Access, Not Credit

ZivoAdvance® is Earned Wage Access (EWA): a product that allows workers to access wages or income they have already earned before their next scheduled payment date. The consumer is not borrowing money they have not yet earned; the consumer is accessing a portion of the consumer's own earned income early, subject to verification and product rules. ZivoAdvance® is not a payday loan, personal loan, line of credit, or deferred presentment transaction under Chapter 560, Part IV, Florida Statutes.

Rise does not extend credit within the meaning of the Truth in Lending Act (TILA), Regulation Z (12 C.F.R. Part 1026), or comparable state consumer lending statutes, because ZivoAdvance® provides access to already-earned income rather than a right to defer payment of borrowed principal on credit terms. This position is consistent with the Consumer Financial Protection Bureau Advisory Opinion published at 90 Fed. Reg. 60070 (December 23, 2025), which confirms that properly structured earned wage access products, including direct-to-consumer models, are not credit within the meaning of TILA and Regulation Z. TILA credit disclosures such as Amount Financed, Finance Charge, and annual percentage rate do not apply to ZivoAdvance® as currently structured.

Product Specifications, Amounts, Fees, and Limits

ZivoAdvance® offers fixed advance amounts of fifty dollars ($50.00), seventy-five dollars ($75.00), or one hundred dollars ($100.00). Only one outstanding advance may be active at any time per consumer; this limit is system-enforced. Rise charges a flat fixed service fee for each advance. There is no interest, no annual percentage rate, and no time-based finance charge that accrues based on the amount advanced or the duration the advance remains outstanding.

All fees, limits, and pricing applicable to a consumer's account are disclosed in the Zivo: Cash Advance application before the consumer confirms an advance. Marketing on this website does not state dollar amounts because terms may vary and may change over time. Consumers must review in-app disclosures at the time of each transaction.

Verification, Open Banking, Open Payroll, and Data Partners

Access depends on verification of earned income, linked bank account status, pay-cycle timing, and other risk factors. Not all applicants qualify. Rise uses open banking and open payroll integrations, principally Plaid for account and income verification and Pinwheel for payroll connectivity, together with such other data partners and suppliers as Rise may engage from time to time, to confirm earned or accrued income and to schedule repayment aligned with the consumer's paycheck and pay cycle.

Third-party providers operate under their own terms and privacy policies when a consumer connects accounts or authorizes data access. Rise does not control third-party system availability, data accuracy, or API capabilities. Verification outcomes, repayment scheduling, and availability of payroll-linked repayment options may depend on employer participation, payroll processor support, banking holidays, and network interruptions. Partner data is used for income and cash-flow verification and paycheck timing, not as a substitute for traditional credit underwriting.

Funding, Disbursement, and Repayment Mechanics

Advance funds are typically delivered to the consumer's linked bank account via automated clearing house credit from Rise's operating funds. Advances may be processed through sponsor-bank arrangements, including Bank of America, N.A., where applicable. Repayment is scheduled on a date aligned with the consumer's pay cycle, derived from open banking and open payroll data subject to partner availability. The specific repayment date and total collection amount are disclosed in the application before the consumer confirms the advance.

The primary repayment method is automated clearing house debit from the linked bank account on the scheduled date. Where the consumer elects a supported open payroll repayment option and employer or payroll application programming interfaces permit, repayment may instead be satisfied via employer or payroll-processor settlement on payday. Availability of advances, amounts, and timing are not guaranteed. Service interruptions, bank holidays, verification delays, or account status may affect access to funds.

No Credit Underwriting, No Credit Bureau Reporting

Rise does not access consumer credit reports, does not use credit scores, and does not perform traditional credit underwriting in connection with ZivoAdvance®. Verification is income- and cash-flow-based, not creditworthiness-based. Rise does not report ZivoAdvance® transactions to Equifax, Experian, TransUnion, or any other consumer reporting agency. Credit bureau reporting is expressly prohibited under Rise's Terms of Service.

Non-Recourse Structure and Prohibition on Collections

ZivoAdvance® is structured on a non-recourse basis. If a consumer does not complete repayment, Rise does not pursue that consumer through debt collection, sale of debt, legal action, wage garnishment, or any third-party enforcement mechanism. Rise absorbs non-repayment risk as a product design feature. Rise's sole remedy for non-repayment is to suspend or withhold future advances, subject to product rules in the application.

This non-recourse structure is material to Rise's position that ZivoAdvance® is not a loan or credit instrument and is antithetical to check-based deferred presentment models that contemplate recourse when an instrument is dishonored.

Florida Chapter 560 — Deferred Presentment Classification

Rise's regulatory position is that ZivoAdvance® does not constitute a deferred presentment transaction under Section 560.402, Florida Statutes, and that Section 560.125 is not applicable to Rise's ZivoAdvance® activity as currently structured. Florida's deferred presentment regime governs businesses that exchange currency for a consumer's check and agree to hold that check for a deferment period. Section 560.402(3) defines deferred presentment as providing currency or a payment instrument in exchange for a drawer's check and agreeing to hold the check for a deferment period.

ZivoAdvance® fails each element of that definition. Rise does not accept, receive, or hold a check from the consumer. No payment instrument is tendered by the consumer to Rise in exchange for the advance. Rise does not agree to hold any instrument for a deferment period, and the flat service fee is not a fee charged for deferring presentment of a check. The consumer is not a drawer in the statutory sense. Rise's conclusion is that a product cannot be a deferred presentment transaction without a check.

Money Transmission Classification Under Section 560.103

Florida Statute Section 560.103 defines a money transmitter as a person who receives currency or monetary value for the purpose of transmitting that value to another location or person. Money transmission requires acting as an intermediary handling someone else's money and routing it at the sender's direction. In a ZivoAdvance® transaction, Rise transfers its own funds to the consumer on advance and collects repayment owed to itself on repayment. Rise is the payer on advance and collects its own receivable on repayment. There is no third party whose funds Rise holds or transmits. Rise's analysis is that this principal-in-both-legs structure is not money transmission under Section 560.103.

Federal Earned Wage Access Framework — CFPB Advisory Opinion

The CFPB Advisory Opinion published at 90 Fed. Reg. 60070 (December 23, 2025) establishes a federal interpretive framework for earned wage access products. While not binding on states, it is persuasive authority on whether properly structured EWA products resemble credit subject to TILA and Regulation Z. The 2025 Advisory Opinion confirms that covered earned wage access products, including direct-to-consumer models, can be categorically different from consumer lending when they provide access to already-earned wages, do not perform traditional credit risk assessment, prohibit credit bureau reporting, and limit recourse to withholding future advances.

Repayment mechanics may vary by transaction. Where a consumer elects supported open payroll repayment and employer or payroll processor capabilities permit settlement on payday, repayment may follow a payroll-process path. Where that path is unavailable or not selected, repayment more commonly occurs by automated clearing house debit from the linked account on a pay-cycle-aligned schedule. The 2025 Advisory Opinion's relevance to TILA classification may depend on the actual repayment path in use; it does not alter Rise's Chapter 560 analysis, which turns on the absence of a consumer check.

Florida Legislative Context and Regulatory Engagement

Earned wage access is a developing product category in Florida. The 2024 and 2025 Florida legislative sessions saw introduction of bills that would have created a purpose-built earned wage access registration framework separate from deferred presentment, money transmission, and consumer lending statutes, including construction language that EWA fees would not be considered interest or finance charges and that compliant EWA providers would not be considered creditors, debt collectors, lenders, or money transmitters under existing Chapter 560 provisions. Those bills did not become law as of the date of these disclosures.

Rise supports enactment of a Florida EWA registration framework and will register under any such law upon enactment. Rise engages constructively with regulators and supervisory authorities on product facts and disclosures, including the Florida Office of Financial Regulation, and responds promptly to inquiries with written submissions explaining product structure and legal classification.

Sections 13 through 15 — including CFPB advisory opinion alignment, Florida Chapter 560 analysis, legislative context, and related documents — are published in the full Zivo disclosures notice.

Rise Digital Financial Corp · EIN 33-1515888 · May 2026

Rise platformFull disclosuresTerms of ServicePrivacy PolicyCompliance

What people say in the stores

Real App Store reviews — shared as written by people who use Zivo.

$25–$200

Grows as you use it

Same-day

When eligible

3 ways

To repay on payday